The Hungarian Mortgage Propaganda

The Swiss Franc Trap and Legalized Borrower Exploitation

Hungarian banks not long ago sold citizens the dream of affordable homeownership through Swiss franc mortgages—only to turn them into lifelong debtors. This essay reveals how banks profited, how governments staged “solutions,” and why the 2025 CJEU ruling C-630/23 could finally upend the system.

Homeownership is Hungary’s Holy Grail.

Hungarians don’t just like to own homes — they worship them. After centuries of losing land to empires, wars, and politics, a house isn’t just a roof here. It’s a shrine to security. That’s why 92% of Hungarians own their homes, one of the highest rates in Europe.

But in the early 2000s, banks found a way to weaponize this cultural obsession. They dangled foreign currency (FX) mortgages — loans denominated in Swiss francs (CHF) or euros (EUR) — that looked like a ticket to middle-class heaven. Glossy ads. Cheerful bankers. Numbers that made regular forint (HUF) mortgages look like daylight robbery.

And we believed them. Why wouldn’t we? When the priest, the banker, and the politician all sing from the same hymn sheet — trust authority, obey the experts — who dares hum another tune?

The Pull and the Push: How to Sell a Trap

The pull: 5–7% lower interest rates compared to standard HUF loans. CHF loans were cheaper because Switzerland had lower interest rates than Hungary.

The push: TV spots and ads where a banker told you, “Your income doesn’t matter — just your property.”

Let that sink in. Your income didn’t matter. Only your house did. Because to the banks, you weren’t a borrower. You were collateral wrapped in skin.

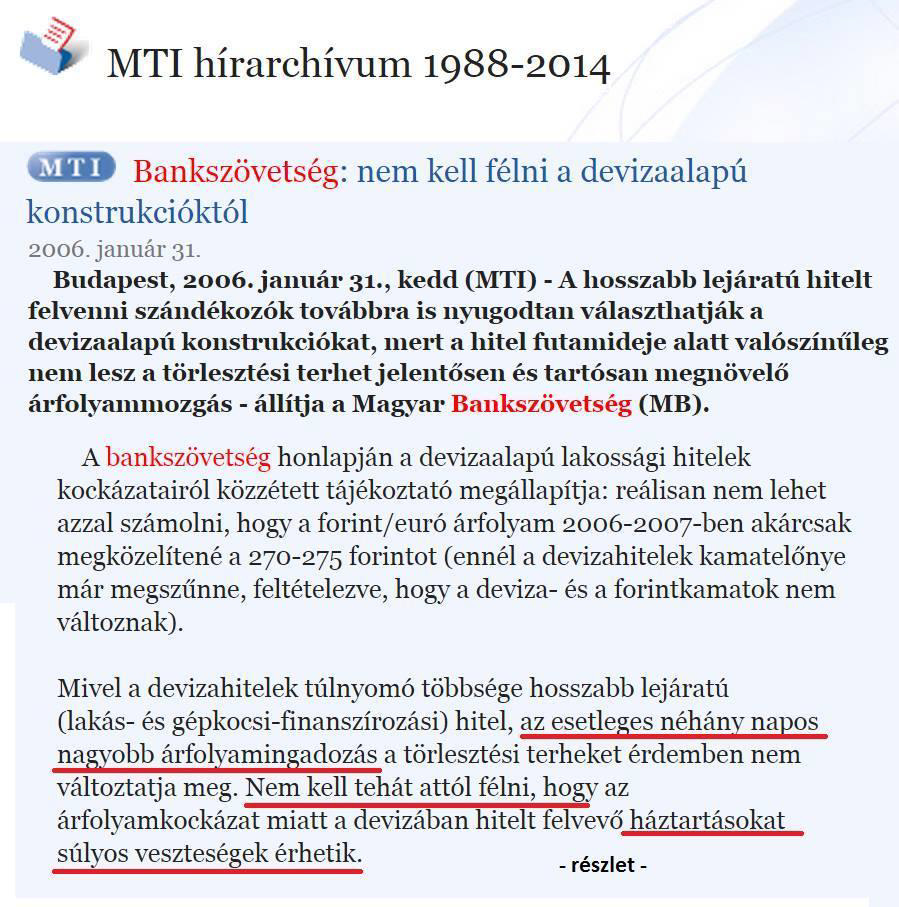

The Hungarian Banking Association even went on record in 2006, assuring people that the forint would never weaken beyond 270–275 HUF/EUR. Spoiler: it tanked to nearly 330. That wasn’t just a bad forecast — it was the financial equivalent of a doctor prescribing cigarettes for a cough.

FX mortgages became the preferred option promoted by both the financial and political systems. The entire banking industry pushed a very aggressive mortgage propaganda.

How Banks Profited — Twice

Every FX loan was a magician’s trick:

You applied in forints (HUF, Hungary’s national currency).

You were approved in forints.

You were told the numbers in forints.

Then — abracadabra! — at contract signing, your loan turned into a Swiss franc chimera.

At disbursement, Banks converted francs to forints at below-market rates, padding their pockets. For Repayment, your forints were reconverted to francs at worse rates, gutting your repayment power.

Profit in. Profit out. All legal. All applauded.

And if the forint strengthened?

Many banks hedged both ways. That wasn’t risk management — that was you betting on both horses and still losing.

Government’s Pseudo Steps — Orchestrated Theater

When the Swiss central bank unexpectedly allowed the franc to jump, it rattled Central and Eastern Europe, with Poland and Hungary hit hardest as countless franc-denominated mortgages became unserviceable and family budgets were thrown into disarray.

The Hungarian state didn’t bungle the FX mortgage crisis. It choreographed it.

Between 2011 and 2015, instead of letting courts enforce EU consumer protection rules (i.e. EU Directive 93/13/EEC on unfair terms in consumer contracts) provides that contracts with unfair terms are not binding on consumers, and unfair terms must be removed (they “shall not bind the consumer”), with certain consequences, the government staged a series of “solutions” that looked good on paper but were theater for the cameras:

Fixed-Exchange Windows (2011): Only the wealthy could participate. If you had cash, you got temporary relief. If not, you got a front-row seat to your own financial funeral.

2015 Conversion: Foreign-currency mortgages were converted to forints at prevailing market rates — after the forint had fallen 73%. Borrowers absorbed the entire loss. Banks smiled. Politicians called it a solution.

The result? Families who had repaid more than the original loan still owed the same amount. The government didn’t fail to protect citizens — it ensured banks could never fail on its watch.

In Hungary, “helping people” meant legalizing the FX scam, going against the EU consumer protection rules and blocking all legal remedies. That’s not incompetence. That’s prioritizing profit over people, then dressing it in bureaucratic respectability.

Poland vs. Hungary: Same Storm, Different Boats

Poland faced the same FX mortgage tsunami, but its courts, not politicians, handled significantly better the fallout. By 2025, nearly 190,000 lawsuits had been filed there, many ending with borrowers recovering real money.

Hungary? The government blocked legal avenues, staged “pseudo-solutions,” and declared the matter closed. Justice wasn’t delayed here — it was abolished by decree.

The New Game-Changer: Case C-630/23

On April 30, 2025, the Court of Justice of the European Union (CJEU, Case C-630/23) dropped a bomb. It declared:

Contracts that dump all currency risk onto uninformed consumers are unfair.

Removing the unfair term isn’t enough — restitution must restore the consumer to the pre-contract position.

Partial refunds? Not acceptable. Crumbs don’t fix decades of policy negligence.

If this ruling is enforced in Hungary, the FX mortgage saga isn’t history — it’s a live wire. Thousands of cases could be reopened. Banks could face massive paybacks. The government’s 2015 “grand solution” could be exposed as unlawful window dressing.

The Bottom Line — How a Generation Was Sold Out

Hungary didn’t just mismanage FX mortgages. It mis-sold reality itself.

Foreign-currency loans were marketed as opportunity. In truth, they were a masterclass in shifting risk while preserving profit. Borrowers became collateral, contracts were traps, and governments acted as referees only for the winning team: the banks.

When the 2008 crisis hit, the Swiss franc appreciated by more than 70% against the forint. Families were crushed. Banks collected hidden spreads. Government “remedies” arrived too late or excluded the majority.

Poland chose courts over decree. Hungary chose legislation over justice.

The C-630/23 ruling proves one thing: the contracts may be old, the propaganda stale, but the injustice is still alive. Hungarians didn’t just buy homes. They subscribed to a system designed to bleed them slowly.

Will Hungary seize this chance to correct history, or double down on the narrative that everything was done “for the people”?

Disagree? Good. I don’t write to be right—I write to be tested. Bring your “Tenth Man” view, your sharpest counterpoint, or even a quiet doubt. Sometimes the most useful critique is the one that unsettles my own thinking.

Don’t forget to subscribe for more Critical Hungary Insights!

Notes for Foreign Readers

HUF: Hungarian forint, Hungary’s currency.

FX mortgages: Loans denominated in foreign currencies (CHF or EUR).

CJEU: European Union’s highest court. C-630/23 is a landmark ruling on unfair consumer contracts.

Polish comparison: Shows a neighboring country addressing FX mortgages with legal recourse rather than political decree.